Written by: Jay Yi, MBA; Edited by: Chris Thompson, CFA, MBA, P.Eng

eResearch | In August, Mastercard (NYSE: MA), a multinational financial service corporation, announced that it will acquire Denmark-based Nets Group, a payments platform that will be leveraged to support faster Business-to-Business (B2B) payments.

In a 2005 corporate strategy decision, Mastercard declared “war” on physical payments and has since been strategizing to take the market lead in replacing cash by digital payments on a global scale. Investments were first made in building the infrastructure and technology to facilitate automated business to consumer (B2C) transactions, which increased the speed of payments, reduced administrative needs, and provided transparency by allowing parties to track transactions.

In September 2018, Mastercard realized the need for a platform to support business to B2B transactions and announced a partnership with Microsoft to jointly develop Mastercard Track, a cloud based B2B payment automation platform that manages identities, compliance, and transactions.

![]() Mastercard’s focus on targeting the B2B payment market is further supported by its recent acquisition of Nets, which is an innovative platform for B2B payment transactions. Nets that has partnered up with over 400,000 merchants, including 35,000 online merchants, more than 240,000 enterprises, and over 240 banks across the Nordic region and mainland Europe.

Mastercard’s focus on targeting the B2B payment market is further supported by its recent acquisition of Nets, which is an innovative platform for B2B payment transactions. Nets that has partnered up with over 400,000 merchants, including 35,000 online merchants, more than 240,000 enterprises, and over 240 banks across the Nordic region and mainland Europe.

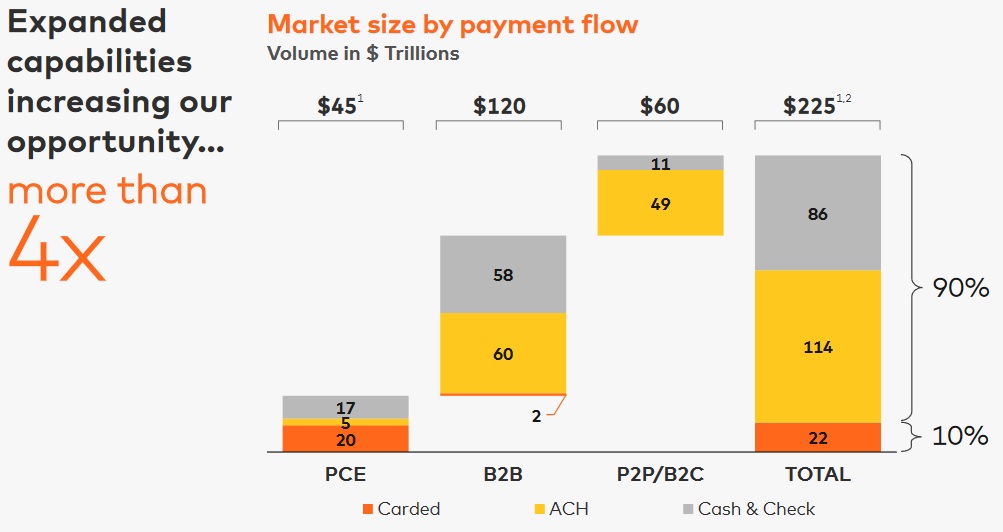

According to Deloitte, in the U.S., the small and medium enterprise (SME) market has revenues of over US$6.6 trillion and is leading economic growth, but while there is infrastructure and intermediaries that facilitate fast transactions between consumers and businesses (B2C), there is a lack of support for B2B transactions.

B2C transactions are in real-time as credit card companies handle 24,000 transactions per second and mobile payment products such as Apple Pay makes it possible for vendors to receive payment right away while third-party companies manage processing of transactions.

B2B transactions, which include businesses working with suppliers or third-party services, take several weeks to process due to lack of support and innovation, which forces corporations to continue using the slow process of drafting checks, getting signatures, mailing payments, and physically processing and reconciling payment data.

Below are some of the downfalls of B2B payments today according to Deloitte:

- High costs: On average, an Accounts Payable organization pays approximately US$8 to process a single supplier’s invoice, and 62 percent of costs stem from manually processing payments.

- Slow processing: It takes an average of 30 days for end to end processing of a payment, and around 47% of suppliers reported delays in payments for their products or services.

- Limited transparency: Once an invoice is sent, there is limited visibility in the end-to-end process of the transaction, and vendors often are constantly calling clients for payment.

- Diverse payment methods: There is no standardization amongst vendors in payment processing methodologies which creates inefficiencies when working with several vendors.

- Reconciliation: Lack of support from financial institutions is forcing manual reconciliation of data and processing of remittance data which is causing a US$3.3 trillion impact.

According to Smithers Pira’s latest market report, non-cash payment transactions are expected to grow 10.5% to 1.96 trillion transactions between 2019 and 2029. B2B transaction management has been a whitespace that has lagged support due to compliance needs and the complexity of multiple parties that need scaled transactions.

Mastercard has been creating a foundation to be the leader in managing all types of payment transactions whether it be B2C or B2B. The Mastercard Track product launched last year, and with the newly acquired Nets platform, it will be interesting to see how many small to medium enterprises use the product to facilitate payments.

//

Mastercard (NYSE: MA)

- Headquartered in New York, United States Mastercard is a multinational financial services company with its primary business in managing payments between banks of merchants and the card issuing banks or credit unions of purchasers.

- Mastercard currently trades at US$291.40 per share with a market capitalization of US$292.4 billion.

//

//