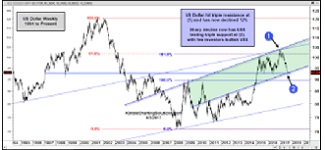

Third Party > Today’s article from Kimble Charting Solutions notes that the Silver rally is approaching a crossroads and is at “triple breakout resistance”. If Silver can continue to rally, it could break out of a 2-1/2 year falling channel. This would be very bullish, not just for Silver, but also for Gold and the Precious Metals sector.

Bob Weir has over 50 years of investment research and analytical experience in both the equity and fixed-income sectors, and in the commercial real estate industry. He joined eResearch in 2004 and was its President, CEO, and Managing Director, Research Services until December 2018. Prior to joining eResearch, Bob was at Dominion Bond Rating Service (DBRS).