eResearch | Year-to-date, the S&P 500 is up over 6% and that is quite impressive considering it was down 34% in March from its peak in February.

The tech heavy NASDAQ 100 is up over 30% year-to-date with the FAANG stocks leading the charge but the Gold BAANG stocks are outperforming the FAANG stocks.

CNBC’s Jim Cramer popularized the acronym FAANG that refers to five high-profile American technology companies: Facebook (NASDAQ: FB), Amazon (NASDAQ: AMZN), Apple (NASDAQ: AAPL), Netflix (NASDAQ: NFLX), and Google/Alphabet (NASDAQ: GOOG).

Although Google posted a slight decline in second quarter revenue due to a decline in online ad revenue, the other FAANG stocks reported strong double-digit revenue growth with Amazon leading the way with a 47.8% revenue increase year-over-year.

As of today, the FAANG stock prices have outperformed the broader market with the following returns:

| COMPANY | CHANGE (YTD) |

| 36.8% | |

| Apple | 70.0% |

| Amazon | 81.1% |

| Netflix | 51.6% |

| Alphabet | 20.3% |

| AVERAGE | 52.0% |

During the current health crisis, central banks have been flooding the market with liquidity and the world’s monetary systems seem to be on the brink of mass currency devaluations.

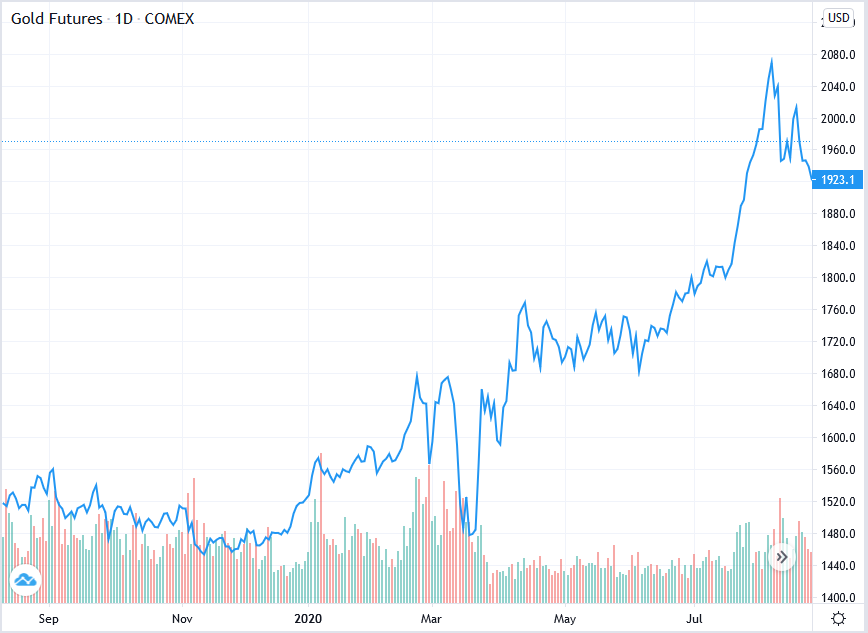

Gold has historically been one of the world’s best store of wealth and a defense against potential devaluation of fiat currencies.

Technical analyst John Roque of Wolfe Research coined the phrase BAANG to refer to a group of gold mining companies: Barrick Gold (TSX: ABX), AngloGold (JSE: ANG), Agnico Eagle Mines (TSX: AEM), Franco-Nevada (TSX: FNV) and Gold Fields (JSE: GFI).

With the price of gold up almost 30% in the past year, profits at the larger mining companies have increased as well.

In the second quarter, Barrick’s revenue was up over 48% year-over-year, followed by Gold Fields up 27.2%, AngloGold up 26.4%, Franco-Nevada up 14.6% and Agnico Eagle up 5.8%.

As of today, the BAANG stock prices have outperformed the broader market and outperformed the FAANG stocks with the following returns:

| COMPANY | CHANGE (YTD) |

| Barrick Gold | 56.9% |

| AngloGold Ashanti | 47.7% |

| Agnico Eagle | 27.6% |

| Franco-Nevada | 44.7% |

| Gold Fields | 115.1% |

| AVERAGE | 58.4% |

As central banks seek ways to stimulate the economy, it creates an environment of negative real interest rate and an increasing amount of government debt with the potential for a weakening U.S. dollar that should help put upward pressure on the price of gold and benefit precious metals mining companies with current production.

CHART 1: Gold Price – 1-Year