eResearch | The energy sector is showing renewed vigor with industry indexes, the price of crude oil, and the Model Oil Portfolio all recording good gains in December.

Portfolio Performance

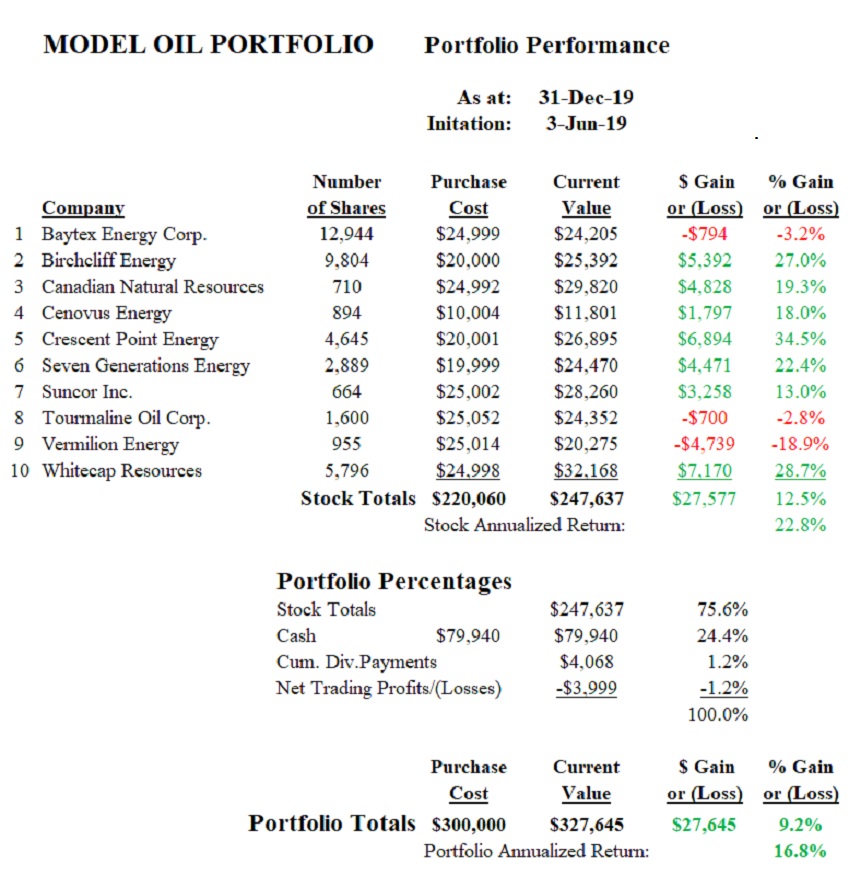

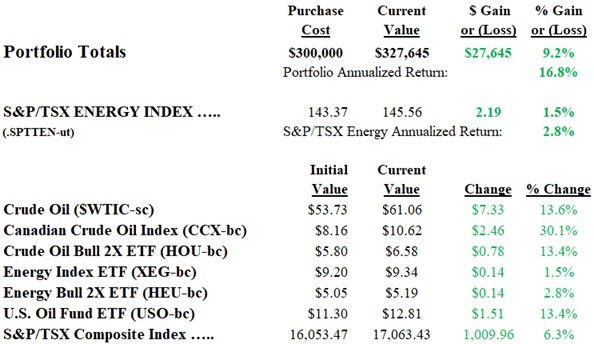

We started our Model Oil Portfolio on June 3, 2019. It struggled mightily right from the get-go, and was “under water” until September 12. It traded in positive territory for just 13 days before going back into the “Red” on October 1. It took until December 10 for the Portfolio to regain a profitable reading, where it has remained ever since, and even reaching its all-time high on the last day of the year. The initial investment was $300,000 and this has grown by 9.2% to $327,645 on December 31.

Portfolio Comparison

For comparison, since June 3, the S&P/TSX Energy Index is up 6.3% and the price of crude oil has risen 13.6%. You can check our overall performance in the tables and graphs set out below.

Portfolio Continues

We will continue with our Model Oil Portfolio in 2020. We expect a continuing recovery in the energy sector and are well positioned to benefit should that occur.

Winners and Losers

The Portfolio continues to record 7 stocks that are in the Green and 3 that are in the Red.

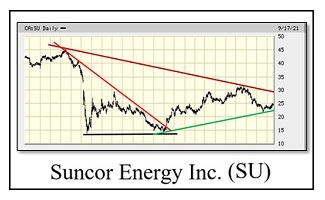

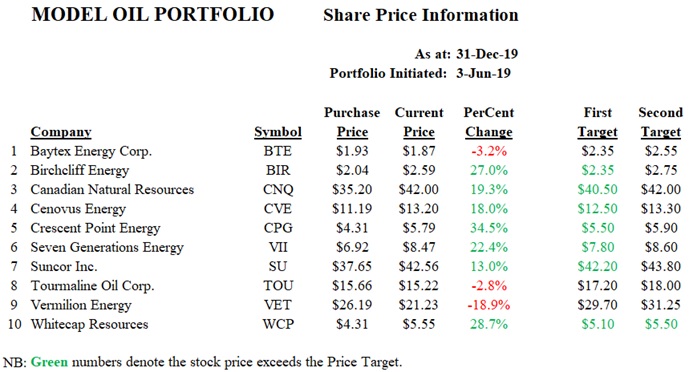

Our best-performing stocks since inception are Crescent Point Energy (up 34.5%) and Whitecap Resources (up 28.7%). Honourable mention goes to Birchcliff Energy with its 27.0% gain since its addition to the Portfolio on just November 1.

Our three laggards continue to be Vermilion Energy (down 18.9%), Baytex Energy (down 3.2%), and Tourmaline Energy (off 2.8%). All three are showing some recovery tendencies.

Cash Position

We continue to hold a sizable cash position, currently 24.4% of the Total Portfolio. We will look for opportunities to utilize some of that cash hoard because there are a few of the holdings, notably Cenovus Energy, whose cost basis is well below the others. Also, there is nothing stopping us from adding new names to the Portfolio since it is not confined to 10 stocks. However, the maximum single holding on a cost basis cannot exceed $30,000.

INDUSTRY COMPARISON

Next, the return on the portfolio is compared to various energy bench-marks.

The Portfolio since inception is up 9.2%. The S&P/TSX Energy Index is up 1.5%. The Energy Index Bull 2X ETF (HEU) is up 2.8%. The Energy Index ETF (XEG) is up 1.5%. The price of Crude Oil is up 13.6% and the Canadian Crude Oil Index (CCX) is up a significant 30.1%.

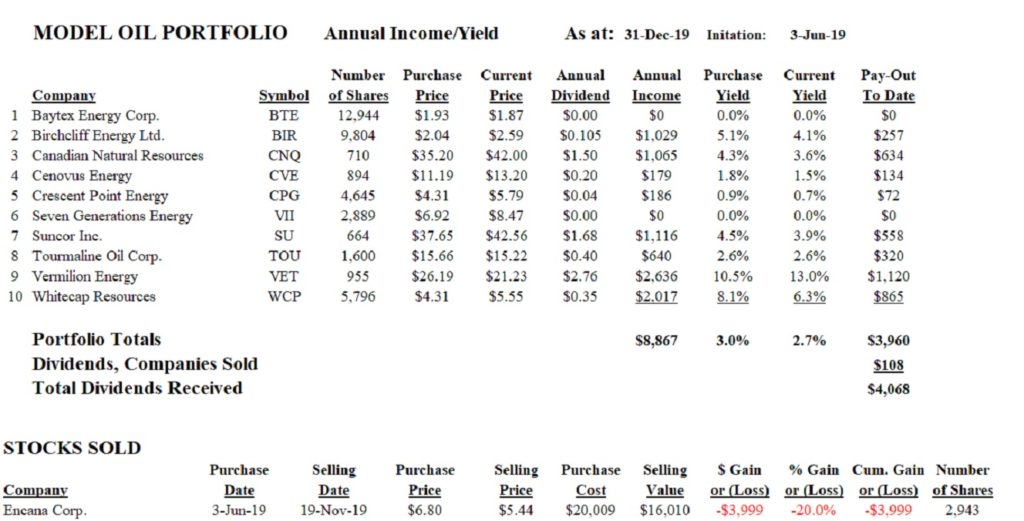

DIVIDENDS and YIELDS

The table below indicates the annual dividend and corresponding annual income and yields. This table is updated twice monthly or when a stock is bought or sold.

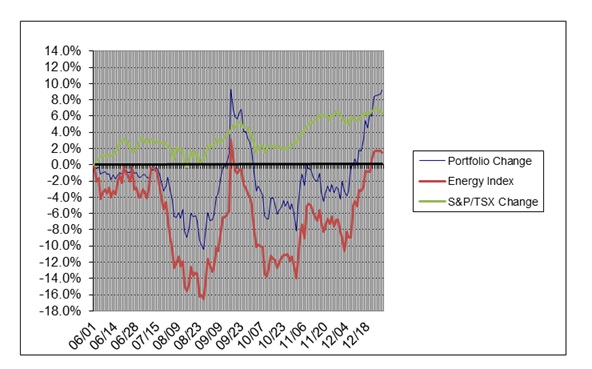

GRAPHIC COMPARISONS

As at: December 31, 2019

Portfolio = +9.2% after dividends and trading losses; +12.5% (stocks only)

S&P/TSX Energy Index = +1.5%

S&P/TSX Composite = +6.3%

//